Chronicle of November 2024

U.S. Equity Outlook 2025

The U.S. stock market has hit a record high, delivering a remarkable 28% total return year-to-date (as of Nov 30), with a historically elevated valuation of 22x forward P/E ratio. Can the bull market charge ahead into next year?

The recent surge in the U.S. stock market can largely be attributed to Trump’s sweeping victory in the Nov 4 election, as evidenced by the accelerated rally in the S&P 500 following election results. Trump's pro-growth policy agenda has bolstered market optimism. However, it’s worth noting that the rally began earlier, around October 2023, when the market started anticipating a dovish pivot from the Federal Reserve and gaining confidence in the sustained decline of inflation.

Despite mixed economic data throughout the period, there is a growing confidence in the resilience of the U.S. economy, with inflation appearing to remain under control. Recent data supports this narrative: nonfarm payrolls exceeded expectations, and disposable income saw notable gains. Consequently, inflation inched up to 2.8% year-over-year, a slight increase but well within consensus expectations.

This economic backdrop comes amid persistent challenges. Concerns about US fiscal policies, including ballooning national debt, the Federal Reserve’s aggressive rate hikes since 2022, and two unresolved major geopolitical crises, remain front and center. Adding to these fears was the looming threat of a recession, which, contrary to widespread expectations, never materialized.

Yet, the S&P 500 continues to climb, repeatedly breaking record highs. The question on everyone's mind is: how long can this momentum last?

It's All About Growth

The Trump effect is undeniably contributing to the rally, especially after the election. Is it justified? We wrote about Trump's programs here and here.

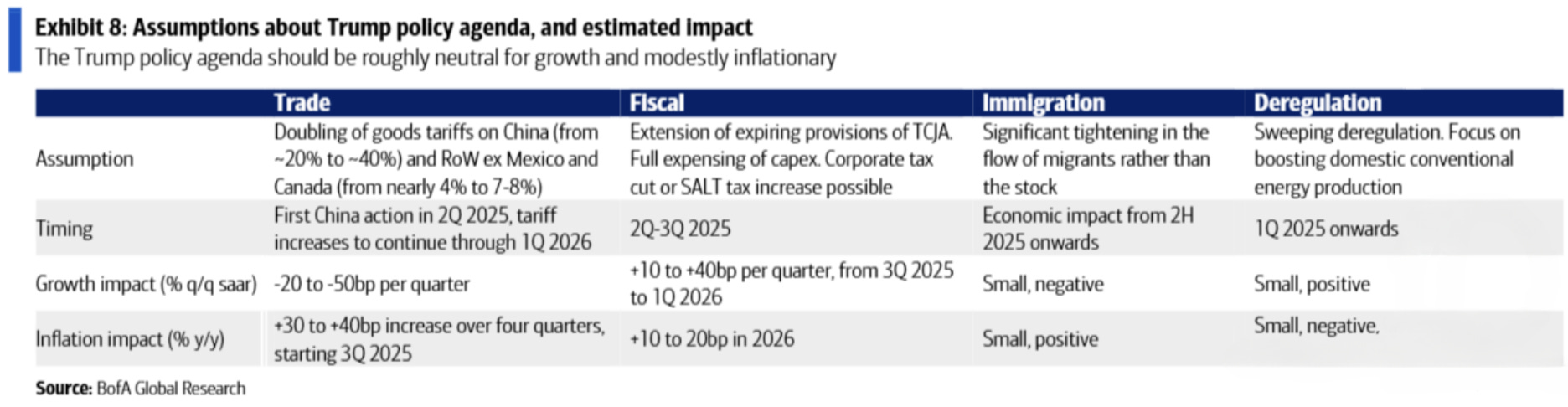

It seems justified for now. Bank of America Merrill Lynch (BoAML) succinctly summarizes their findings in the following table:

Bank of America Merrill Lynch’s (BoAML) view is somewhat constrained, but their "neutral growth" projection essentially suggests that the economy is still on a growth trajectory. According to BoAML, Trump's plan to significantly increase import tariffs could weigh on growth. However, this point is debatable; after all, when Trump raised tariffs in 2019, the US economy continued to grow unabated.

BoAML suggests that any negative impact from higher tariffs will likely be offset by favorable fiscal policies, such as further corporate income tax cuts. Meanwhile, Trump's immigration and deregulation policies present a mixed picture. Although harder to quantify, these policies tend to balance each other out, mitigating their overall impact.

It’s important to note that BoAML’s calculations reflect the marginal growth on top of the current trajectory, with the latest real GDP growth standing at 2.8% year-over-year. Additionally, the benefits of Trump's deregulation efforts are expected to have a more pronounced effect in the long term rather than in the immediate future.

This relatively strong GDP growth trajectory appears modest when compared to corporate growth projections. For example, Goldman Sachs forecasts an 11% year-over-year earnings growth for S&P 500 companies in 2025.

When comparing these earnings growth projections to companies outside the US, it’s easy to see why fund flows are gravitating toward the US market. Goldman Sachs projects European stocks to deliver just 3% earnings growth, Japan 6%, and Asia-Pacific stocks 10% in 2025. With such disparities, why settle for less when the US offers a far more compelling growth trajectory?

It’s important to note that emerging markets come with significantly higher volatility and increased investment risks. Investors typically demand a greater risk premium to compensate for the uncertainties associated with EM growth. This makes the comparatively stable and robust growth of US companies even more appealing.

Valuations are Trickier

It’s fair to acknowledge that historically, after reaching high valuation levels, as measured by the Cyclically Adjusted Price-to-Earnings Ratio (CAPE or Shiller PE Ratio), the S&P 500 has often delivered only mediocre average returns. However, it’s crucial to note that the actual range of returns has been quite broad, occasionally reaching as high as 15%.

This suggests that the S&P 500’s performance next year will likely be driven more by earnings growth than by valuation rerating.

What's the Strategy?

We view the growth expectations and valuation dynamics of the S&P 500 as a compelling opportunity. Over the past few years, including year-to-date, the Mag7 stocks have led the charge, significantly outperforming and leaving the rest of the S&P 500 trailing behind.

This dynamic may shift soon. As the market intensifies its search for growth opportunities, stocks outside the Mag7 and even beyond the S&P 500 could come under greater scrutiny. Among the thousands of stocks outside the S&P 500, many boast significant growth trajectories yet trade at much lower valuations compared to their S&P 500 and the Mag 7 counterparts. This presents a fertile ground for investors seeking untapped opportunities.

While the S&P 500 (which represents large and mega cap stocks) valuation is above 20x forward P/E ratio, S&P 400 mid cap and S&P 600 small cap are still valued at 17x and 16.8x, respectively.