We are in a rare moment where investors are given a long window to buy U.S. equities. Yes, volatility is high, and it scares everyone. But for those who can think long-term, stay disciplined, and ignore the noise, this is a great opportunity.

Volatile market scares away investors

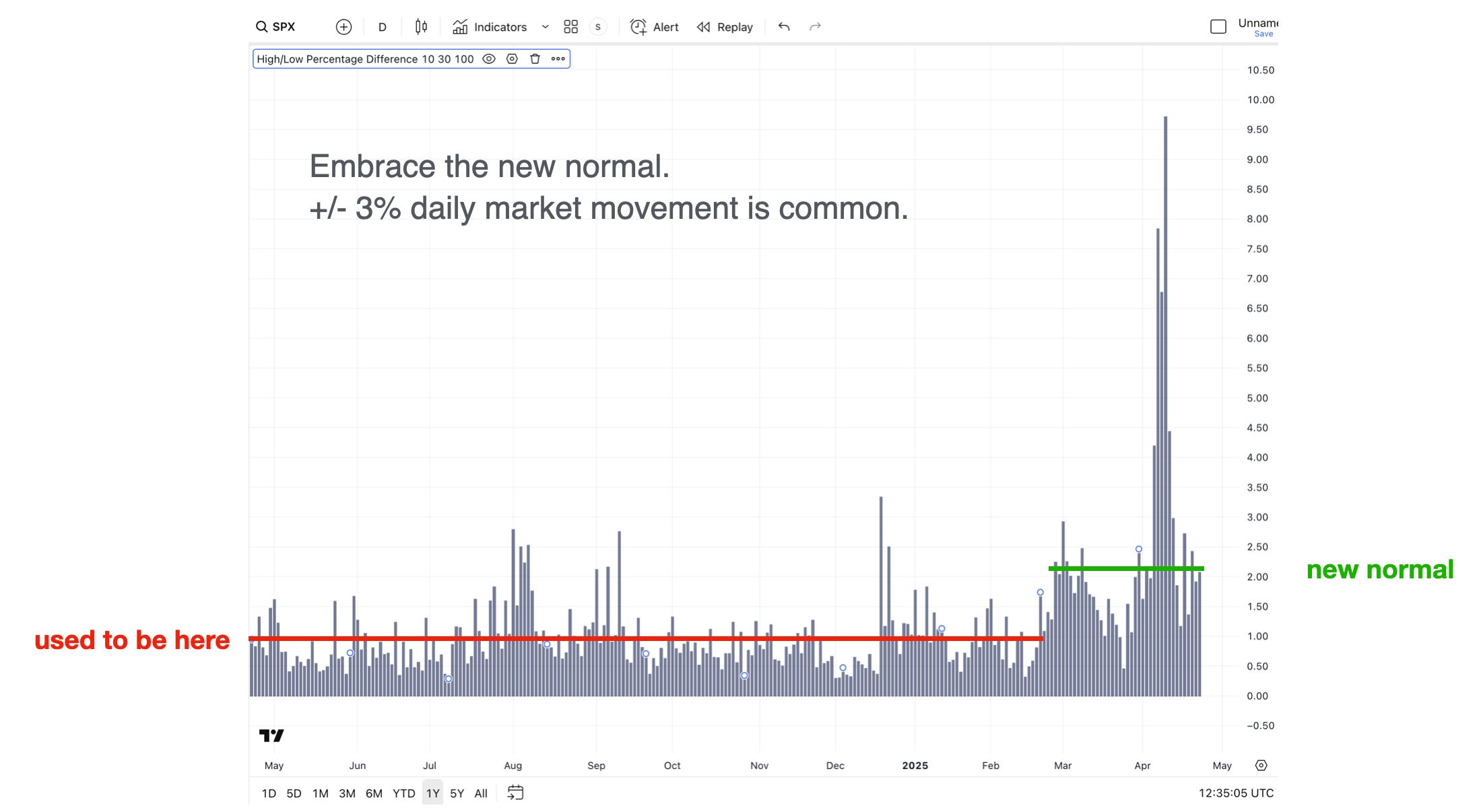

Nowadays, +/-3% intraday moves in major indexes (S&P 500, Nasdaq) are very common. Headlines from Bloomberg, CNBC, and other media are all doom and gloom—about the U.S. economy, stocks, and its future in general. It’s understandable that people feel anxious and avoid taking necessary risks.

This bearishness is reflected across sentiment indicators: AAII Sentiment Survey, CNN Fear & Greed Index, and NAAIM Exposure Index all show extreme levels of negativity. There’s been some improvement lately, but sentiment remains historically bearish.

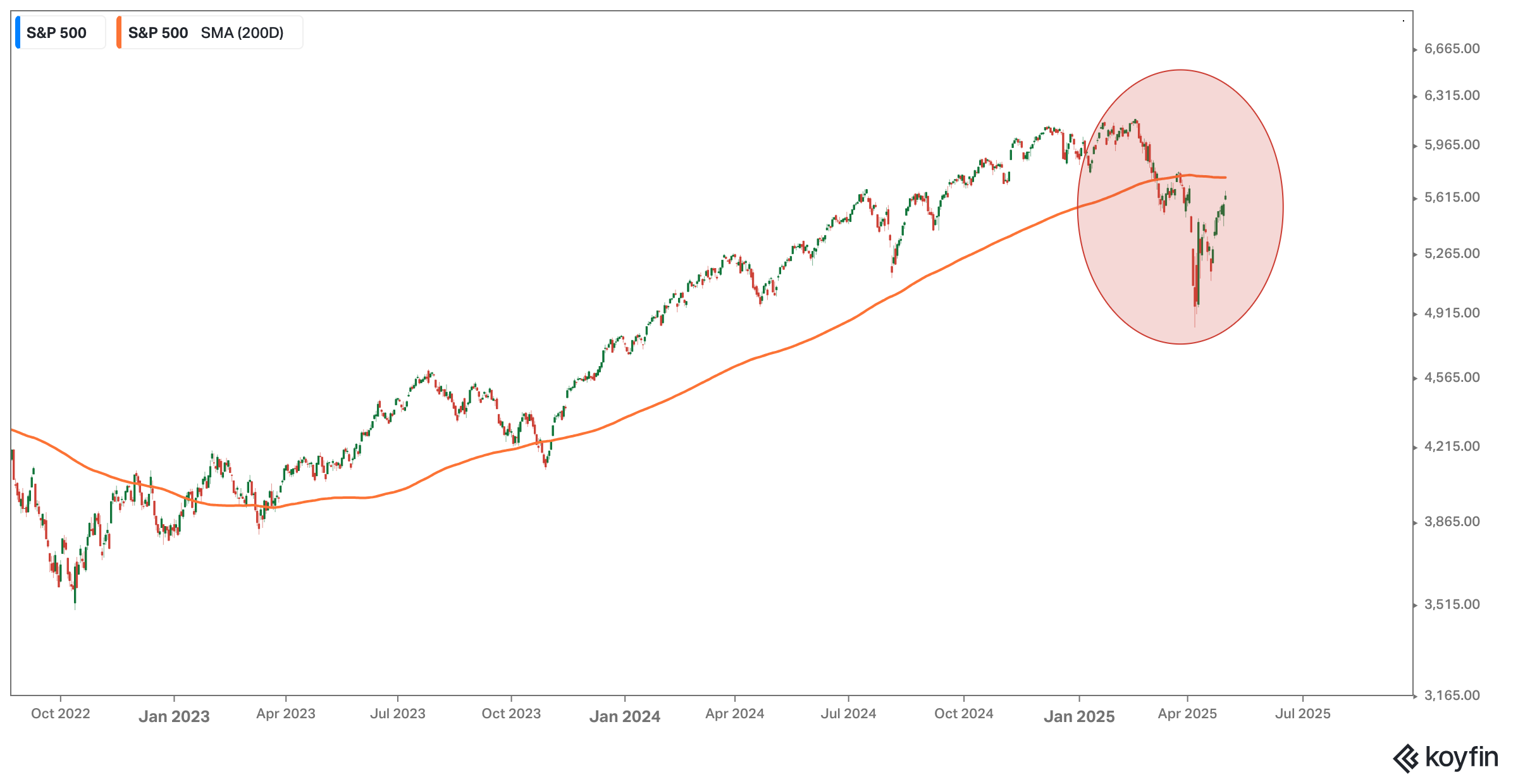

From a technical perspective (note: we do not claim to be experts in technical analysis), major indexes (S&P 500, Nasdaq, Dow Jones) remain below their 200-day Moving Averages. That suggests we are still in a downtrend.

Market is in the process of pricing in the end-game

Buried in the nonstop flow of economic data, Trump tweets, and geopolitical noise, the market is actually trying to price in the end-game of the U.S.–China trade war.

This process will take time, especially as the news flow remains disproportionately negative toward U.S. equities (and U.S. prospects in general). That’s partly why we’re seeing this elevated volatility.

For astute investors, this is a blessing in disguise.

The end-game

The end-game is that the U.S. will come out better off: with more domestic manufacturing, less reliance on Chinese imports, and added national revenue from tariffs.

The common misconception is that tariffs are 100% bad. This ignores the fact that, even before Liberation Day, most other countries already had higher tariffs than the U.S.—despite living in a “globalized” world. And historically, tariffs have had mixed outcomes.

In 1930, the U.S. passed the Smoot-Hawley Tariff while already in a fragile economy. A badly timed Fed rate hike contributed to the Great Depression.

But in 1922, the Fordney-McCumber Tariff was enacted during a strong economy—and U.S. manufacturing soared afterward.

For those who want to explore this deeper, see our CIO interview here.

Contrary to popular belief, these tariffs are not blanket measures. There are curated exemptions—for example: pharmaceuticals, medical devices, semiconductors, automotive parts, and more. This is a calculated strategy—not just “Trump being Trump.”

Moreover, many countries are now eager to negotiate trade deals with the U.S.

Which one will last?

There’s no need to obsess over which country has hypersonic missiles ready to launch. We may never see them used anyway.

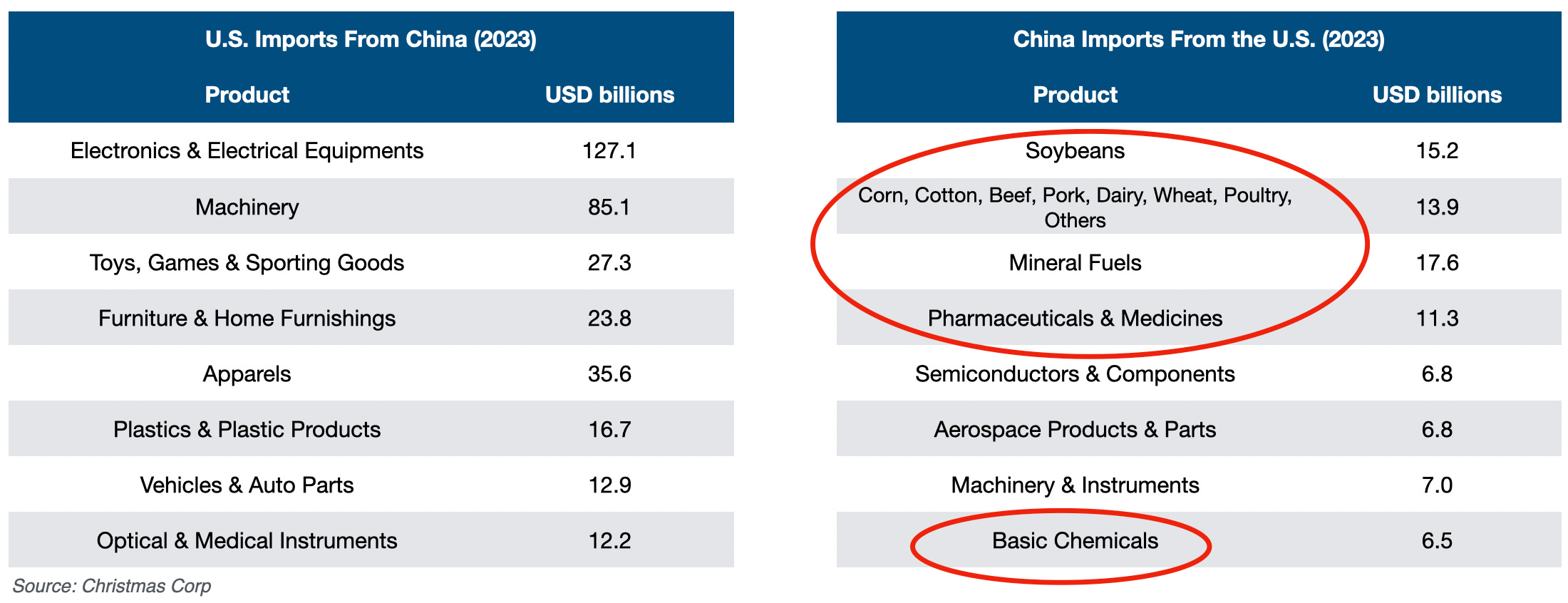

This simple table of top 10 imports gives a much clearer signal. The U.S. imports mostly industrial or secondary goods. China, on the other hand, imports basic necessities: raw food, fuel, and raw materials.

Ironically, Mao Zedong’s quote from the 1930s applies here: "A single spark can light a prairie fire." He used it to criticize how the Communist Party ignored rural populations—warning that small discontent could lead to full-scale upheaval. Today, it’s not just farmers; it’s everyone who needs basic goods to live.

Endless data clouds judgment

Most people today are victims of the nonstop flow of economic headlines and data overload. It clouds judgment and makes them lose sight of the big picture.

Just a few days ago, Q1 2025 GDP was released: it showed a -0.3% contraction, and the U.S. stock market dropped more than -2% in the first few hours. Compared to China’s +5.4% growth, it triggered a wave of recession panic.

But most of the negative GDP came from a surge in imports—businesses front-loading foreign goods ahead of Trump’s tariffs. A large portion of those imports were gold, likely speculative positioning against tariff uncertainty.

The underlying numbers actually show decent consumption growth—something that doesn't happen during a real recession.

Catalysts ahead

Interestingly, all the doom-and-gloom headlines seem to ignore several highly probable positive catalysts ahead.

First, the Fed rate cut is inevitable. Debates over timing and scale are just noise. Everyone agrees on one thing: it will be cut.

Second, any good news on onshoring will serve as a strong catalyst. Many still underestimate American craftsmanship and doubt the country’s manufacturing capability.

Third, tax cuts will lift consumer purchasing power and boost corporate profits. Extensions of the 2017 Tax Cuts and Jobs Act are in play, with the next round likely focusing on individuals.

Fourth, deregulation is also on the table—targeting environmental, financial, and labor rules. This would reduce compliance costs, speed up project approvals, and improve business flexibility.

So, it's time

In April, our portfolio strategy gained +1.20%, while the S&P 500 total return was -0.68%. Our approach remains the same: tilt toward low-volatility stocks and deploy cash tactically during episodes of widespread, unreasonable fear.

We believe we’re entering a stock-picker’s market, where stock selection plays a bigger role in delivering outperformance.

As the year progresses, the window to accumulate quality stocks at bargain prices is narrowing, as the market tries to price in the endgame of the trade war debacle.

Fortunately, for those still underexposed to U.S. equities, volatility remains elevated. Some may choose to wait for the next crash. You might get a better entry point, or this might be it. Nobody, including us, knows for sure.

A new Trump Tower just launched in Dubai a few days ago, with penthouses priced at $20 million. Its brochure features a beautiful quote:

“Good things come to those who wait. Great things come to those who don’t.”

That quote sums up our view perfectly. Waiting for the perfect moment often means missing it. In volatile markets like this, disciplined action—backed by a sound strategy—beats hesitation every time.