Market sentiment has turned sharply cautious, with fears of recession and stagflation dominating the narrative. Yet beneath the surface, corporate earnings remain resilient, and extreme pessimism may provide opportunities.

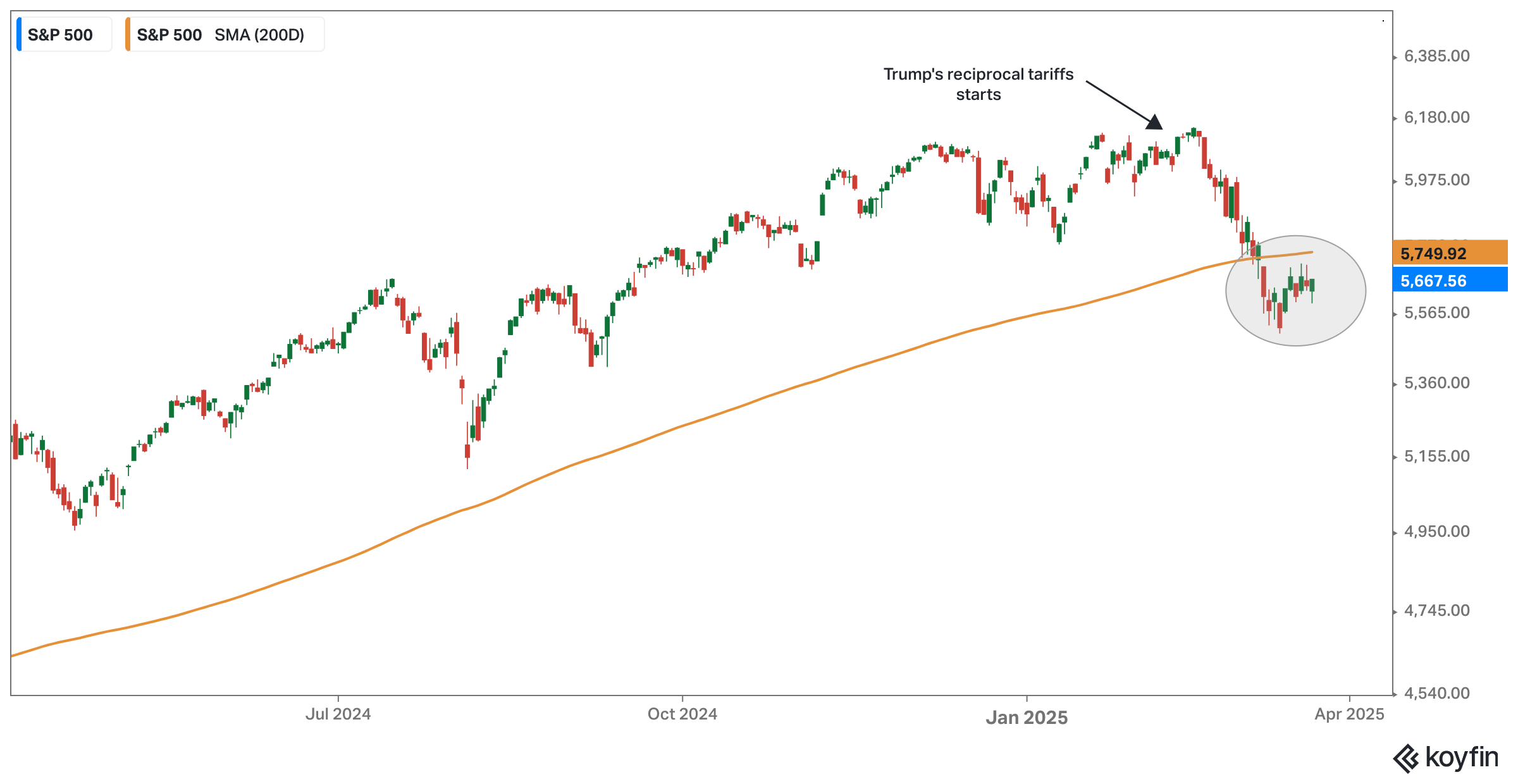

The wall of worry is still present for U.S. equities. Key concerns include persistent recession fears, exacerbated by "Trump Tariff 2.0." Some are even predicting the return of stagflation — a combination of slow growth and high inflation.

Concerns about a recession have persisted since 2022, when President Biden’s Inflation Reduction Act (along with other policies) contributed to higher inflation and prompted the Federal Reserve to raise interest rates by over 4% within a year. That recession, however, has yet to materialize.

Now, recession fears are resurfacing against the backdrop of the Trump Tariff policy. This time, the concern appears more justified, especially in light of the Atlanta Fed’s GDPNow forecast for U.S. real GDP in Q1 2025, which dropped as low as –2.82%.

However, this forecast comes with its own limitations. The Atlanta Fed’s GDPNow model does not adjust for distortions caused by temporary trade shifts or non-economic factors — such as the recent tornado in Texas or wildfires in California. As a result, the model may not fully reflect the underlying strength of the economy.

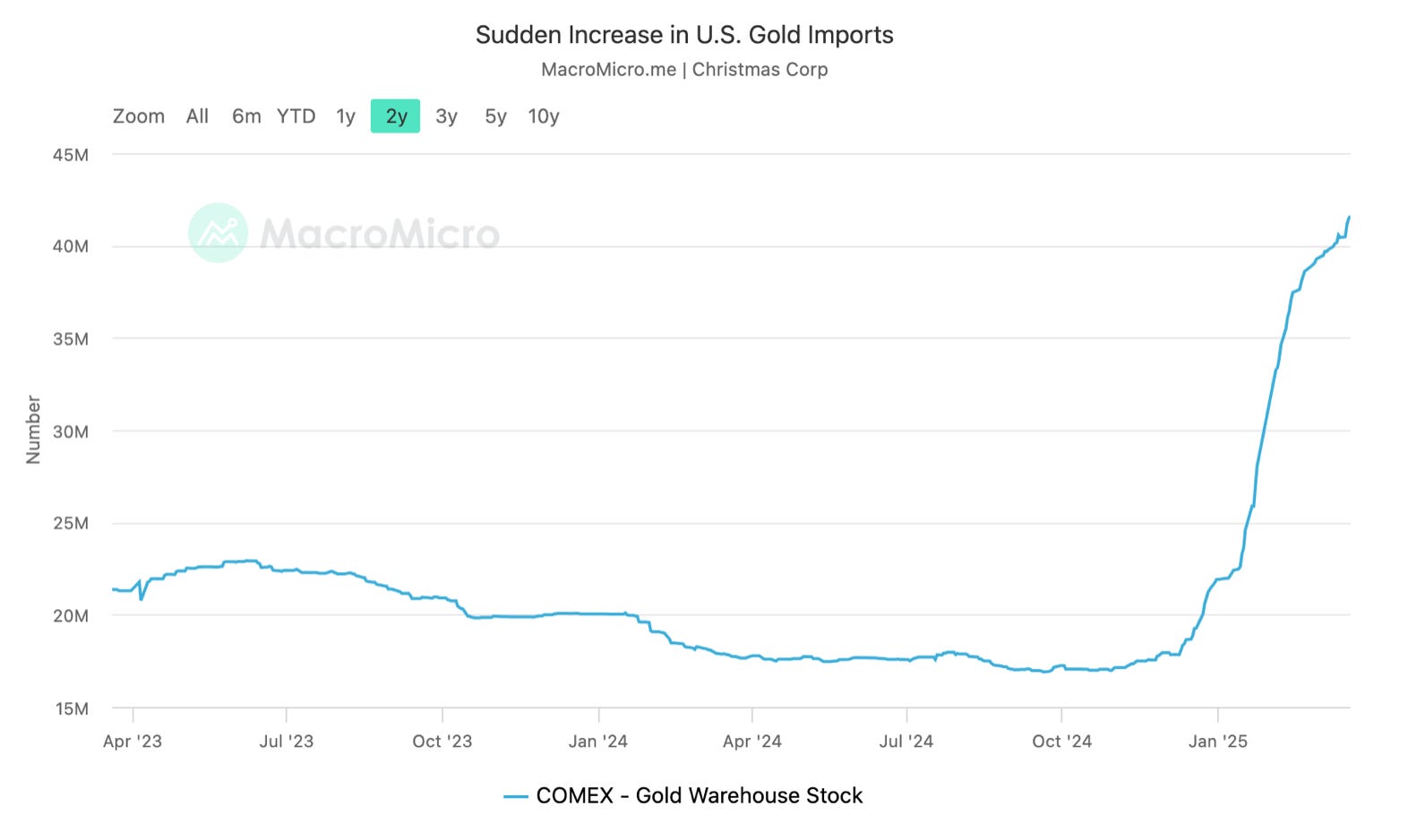

Regarding the trade shift, there has been an unusual surge in U.S. imports during Q1 2025 — driven predominantly by gold. There's been considerable chatter around this phenomenon, and it likely deserves an article of its own. For now, it's sufficient to say that this spike in gold imports has distorted the GDPNow forecasting model.

Worse than a recession, some experts are even forecasting the possibility of stagflation — a scenario where the economy experiences high inflation alongside slow growth. The only significant episode of stagflation in U.S. history occurred in the 1970s, when the term was first coined.

Will it happen again in the near future? That’s a matter for economists to debate. But history shows that stagflation is rare and difficult to trigger.

To be fair, several notable economic indicators suggest that a recession may be looming. One of the strongest warnings comes from the Conference Board’s Leading Economic Index (LEI), which has been deteriorating since early 2022 — a signal that a recession could be on the horizon. It's no surprise, then, that markets are growing increasingly anxious.

Sentiment & Positioning

Predicting where the economy is headed is never easy. In fact, the same economic data can trigger both positive and negative reactions in the market.

While many economic indicators appear gloomy, a more encouraging signal comes from sentiment and positioning data.

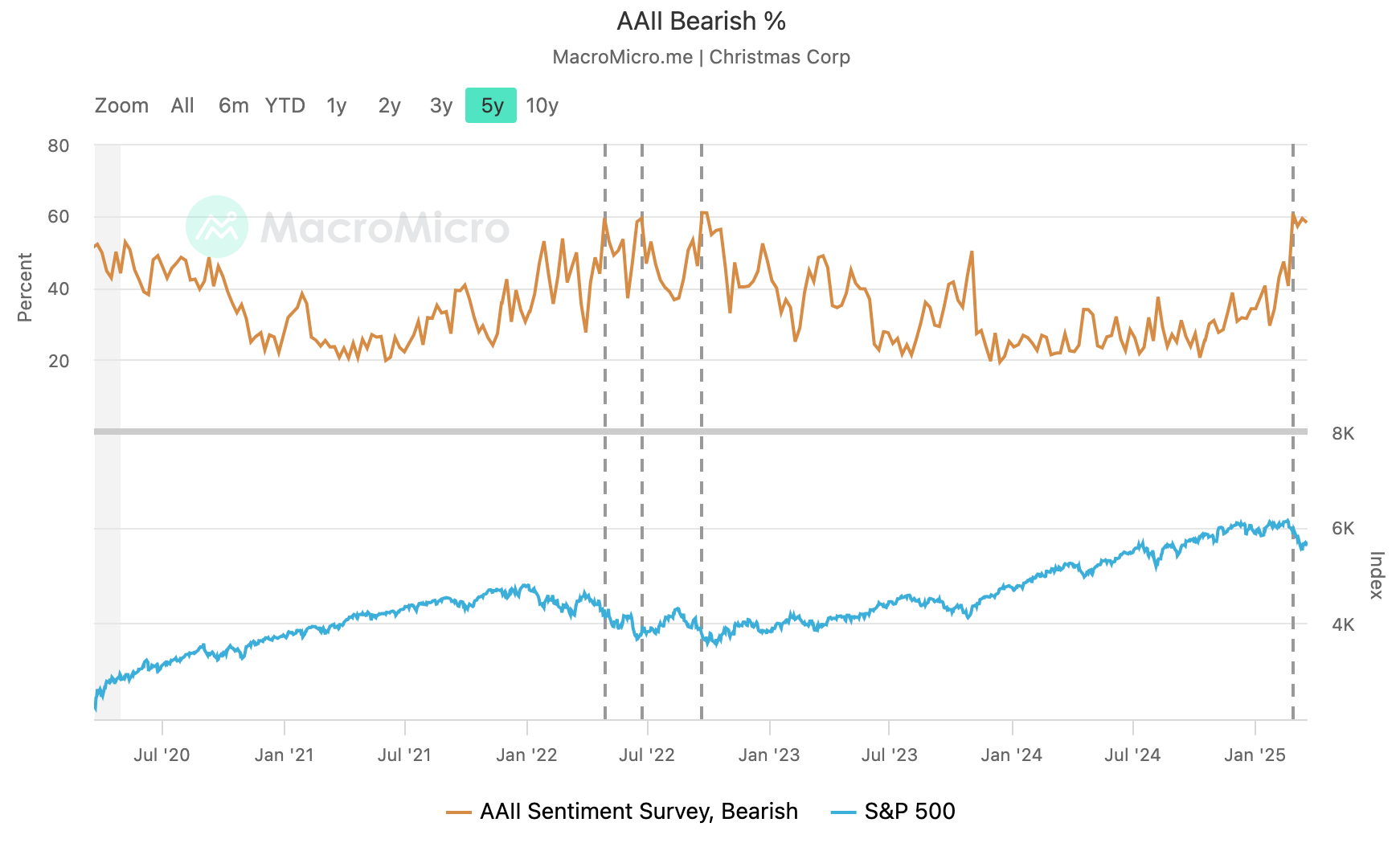

The AAII Sentiment Survey currently shows an elevated level of bearishness among individual investors — and historically, such extremes have often been followed by positive returns in the stock market.

The CNN Fear & Greed Index also reflects extreme fear — a level that has historically been followed by positive returns in the stock market.

The NAAIM Exposure Index also reflects a degree of bearishness, though not as extreme as other sentiment surveys. This suggests that while active investment managers remain cautious, they haven't fully retreated from equity exposure.

Positioning data also points to a bearish tilt. According to Goldman Sachs, CTAs (Commodity Trading Advisors — large and leveraged traders) currently hold a net short position in U.S. equities for the first time since 2023.

And finally, this headline captures what many average investors are thinking about the U.S. stock market right now.

Corporate Earnings

Despite wobbly economic data and bearish sentiment, U.S. corporate earnings remain resilient. Overall, expected earnings for 2025 are still projected to be higher than those in 2024.

The economic disruption from the Trump Tariff has so far made only slight revisions to 2026 earnings forecasts — and it has triggered a market rotation from tech stocks to non-tech sectors.

It appears that the current wave of bearishness has impacted valuation multiples more than earnings. Since mid-January, the S&P 500's price-to-earnings (P/E) ratio has declined from 23.4x to 20.7x.

While the S&P 500’s current P/E level might still be seen as “expensive,” many individual stocks have reached far more reasonable valuations. Take NVIDIA, for example — one of the most loved and, at the same time, most hated stocks in the market.

Happy investing.