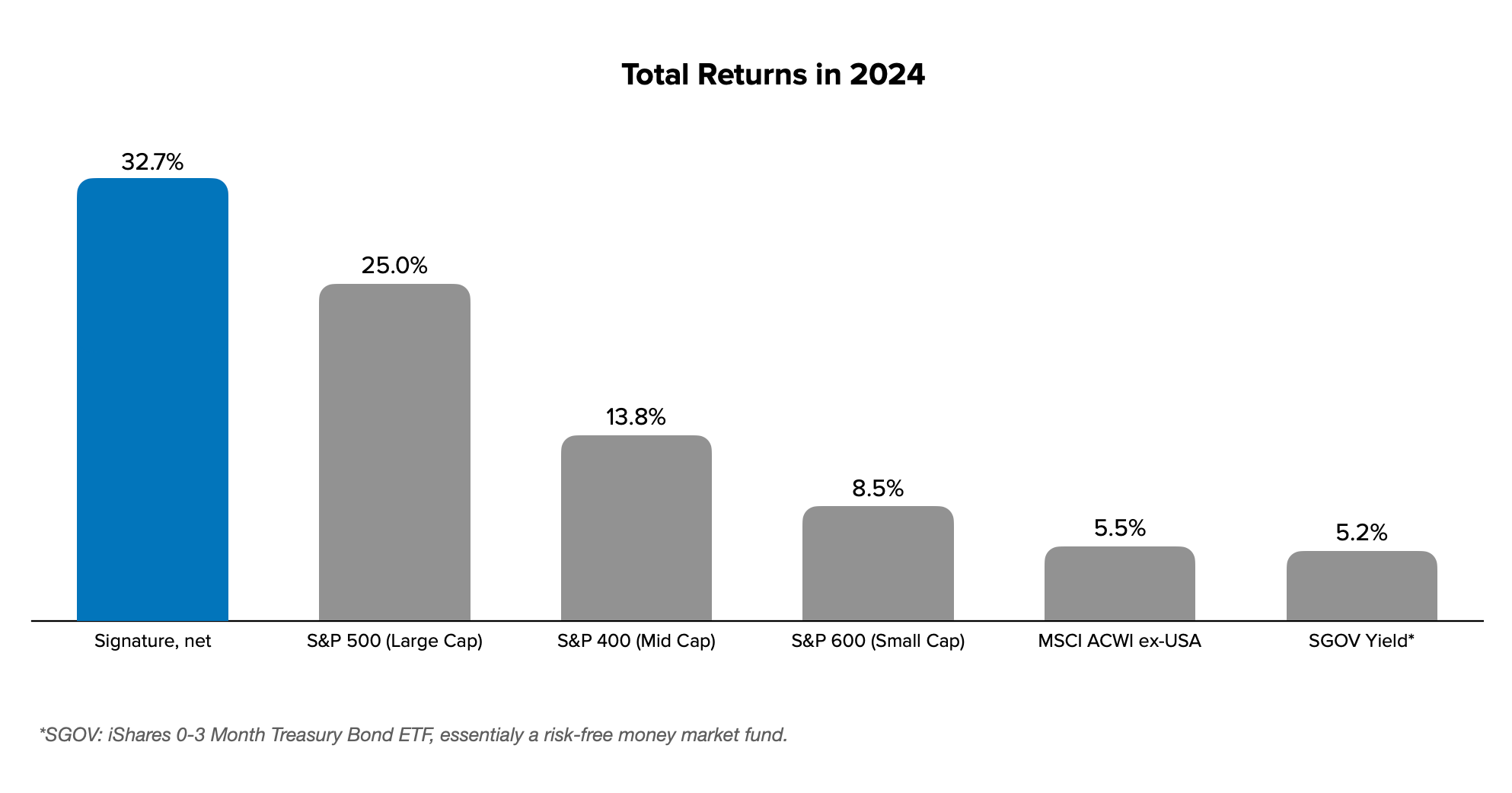

The year 2024 was remarkable, exceeding muted expectations by a wide margin. At the start of the year, consensus forecasts predicted only a modest 5% upside for the U.S. stock market. Instead, the S&P 500 delivered an impressive 25% total return, while our Signature Strategy delivered a 32.7% net return.

If the Christmas Signature Equity portfolio were a hedge fund, here is where the 'fund' would have ranked in 2024:

Note that the majority of our clients are managed using this portfolio strategy.

Review of Signature

As Christmas Signature Equity strategy celebrates its 9-year milestone, explore the journey and discover our unique edge in detail.

Over this period, the portfolio has delivered an impressive 18.4% gross annual return and 16.1% net annual return. This translates to a 3.82x net multiple of invested capital (MOIC) in just nine years.

The presentation highlights key statistics and achievements of our Signature Strategy over its nine-year journey. It showcases top contributors for 2024 and lifetime, emphasizing the strategy's ability to identify and invest in multi-baggers. We explore the factors that set us apart, including our high active shares, patient investment approach, and robust portfolio construction process.

Return is one thing, but risk management is another. Our strategy has consistently delivered best-in-class outperformance with exceptional risk-adjusted returns, supported by low beta and a low downside capture ratio. This balance of growth and risk control makes our portfolio a perfect fit for long-term investors seeking both stability and superior returns. The truth is, if you're already investing with us, you may not need another portfolio!

U.S. Optimism

Two key factors drove the impressive market returns in 2024. First, the highly anticipated Federal Reserve's rate cut in September signaled a shift toward more accommodative monetary policy. While this move will remain subject to debate due to the cyclical nature of economic policy, the second factor was more fundamental: Donald Trump’s landslide presidential victory. This event significantly boosted U.S. confidence, setting a tone of optimism likely to persist for years.

Such optimism in the U.S. stands in stark contrast to the gloomy sentiment across much of the rest of the world. The MSCI ACWI excluding USA index, which comprises large cap and mid cap stocks from 56 countries outside the United States, delivered a 5.5% return in 2024, including dividends. This pales in comparison to the S&P 500's impressive 25% total return. (ACWI: All Country World Index)

To put this in perspective, the yield on ultra-short-term U.S. Treasuries hovered around 5.2% throughout 2024, offering a risk-free return. Consequently, investors who allocated funds to non U.S. markets faced additional risks for returns barely exceeding what they could have earned with a U.S. risk-free investments.

Trump's victory is not just the usual optimism for a newly elected government. Instead, it is an optimism that he will reform the core of U.S. fundamentals, including improving government efficiency, implementing deregulations, and pursuing further reductions of income taxes. The fact that Trump won —seriously, reducing government size is a highly unpopular policy and could be political suicide— makes us believe that U.S. optimism will persist for years to come.

Trump's policies are often intriguing, including his support for Bitcoin and the suggestion that it could become part of the national reserves. While groundbreaking on the surface, the idea isn't entirely new. El Salvador adopted Bitcoin as a national reserve years ago, despite facing significant pushback. Similarly, Texas has recently proposed a bill to establish Bitcoin as a state reserve. With financial institutions embracing Bitcoin and only 5% of it left to be mined, the future of this digital asset appears highly promising.

Stock Selection Matters

Simply allocating more to the U.S. market won't optimize returns without selecting the right stocks.

“Here's to the crazy ones. The misfits. The rebels. The troublemakers. The round pegs in the square holes. The ones who see things differently. They're not fond of rules. And they have no respect for the status quo.”

as Steve Jobs once said in a legendary Apple ad.

Contrary to the belief that active stock selection is obsolete in the age of passive funds, we argue that actively managed portfolios —much like the misfits of today’s investing world— can thrive and deliver superior risk-adjusted returns compared to blindly following the herd into passive funds.

It's tempting to attribute performance solely to index trends. In 2024, the S&P 500, representing large cap stocks, rose by 25%, while the S&P 400 and S&P 600, covering mid cap and small cap stocks, gained by 13.8% and 8.5%, respectively. The simple conclusion might be that large caps outperformed. However, not all large cap stocks delivered superior returns.

The Magnificent Seven (Mag7) stocks (AAPL, AMZN, GOOGL, META, MSFT, NVDA, and TSLA) accounted for about 20% of the S&P 500's total weight but contributed over half of its 2024 return. However, their performance varied significantly. NVDA 0.00%↑ delivered an extraordinary 171% return, while MSFT lagged with a modest 12.1%, underperforming the S&P 500. If you had picked NVDA and avoided MSFT in 2024, your portfolio would have significantly outperformed simply investing in the S&P 500. Stock selection, indeed, matters.

The ultimate question is: which stocks should be selected?

While the market provides no guaranteed answers, it does offer valuable clues. Looking ahead to 2025, consensus estimates suggest a 12.3% total return potential for the S&P 500, while the Mag7 shows a slightly lower potential of 11.6%. However, a more selective approach — focusing on three stocks with the most reasonable valuations within the Mag7 — boosts the total return potential to an impressive 19%. This highlights how stock selection, driven by valuation metrics like the PEG ratio, can amplify returns. For example, NVDA’s 27% projected annual earnings growth over the next three years, combined with its relatively modest 31x P/E ratio, results in a much lower PEG ratio compared to its peers, making it a standout investment opportunity.

Active Shares + Patience = Our Edge

Related to "Stock Selection Matters" above, let’s revisit our discussion about the Signature Strategy.

Our portfolio stands apart with 90%+ active shares, where we take bold positions that differ significantly from the benchmark to outperform. Active shares measure the percentage of a portfolio’s holdings that differ from the benchmark index.

Furthermore, our 52% annual portfolio turnover rate is relatively low. It reflects a patient investment strategy, ensuring that each decision aligns with long-term value creation rather than short-term market fluctuations. Portfolio turnover refers to the percentage of a portfolio’s holdings that are bought or sold within a given year. Higher turnover reflects shorter holding periods, while lower turnover indicates longer holding periods. For context, the average turnover ratio for actively managed U.S. stock funds was 63% in 2019. In other words, our holding period for stocks is significantly longer than that of most U.S. funds, reflecting our patient investment approach.

A study by Cremers and Pareek (2016) finds that high active share portfolios combined with patient holding positions (low portfolio turnover) outperform benchmarks by over 2% annually.

Make Signature Great Again

Between October 2016 and October 2020, our strategy significantly outperformed the S&P 500, thriving under the pro-business policies of the Trump administration. Tax cuts, deregulation, and strong corporate earnings created an ideal environment for actively-managed portfolios and sector-specific strategies. This period highlighted the strength of our methodology, allowing us to deliver consistent outperformance in a growth-oriented market climate.

Looking ahead, the 2024 election results bring renewed optimism. We are well-positioned to capitalize on future opportunities, regardless of the macroeconomic landscape. Our commitment to identifying high-quality stocks and delivering long-term value remains unwavering, and we are optimistic about leveraging our strategy to navigate the next four years successfully.

You can always get an updated factsheet here.