Chronicle - May 13, 2025

What Next & Meme of the Century

The S&P 500 is up more than 12% since our Unpopular Opinion piece on April 11, 2025. What’s next?

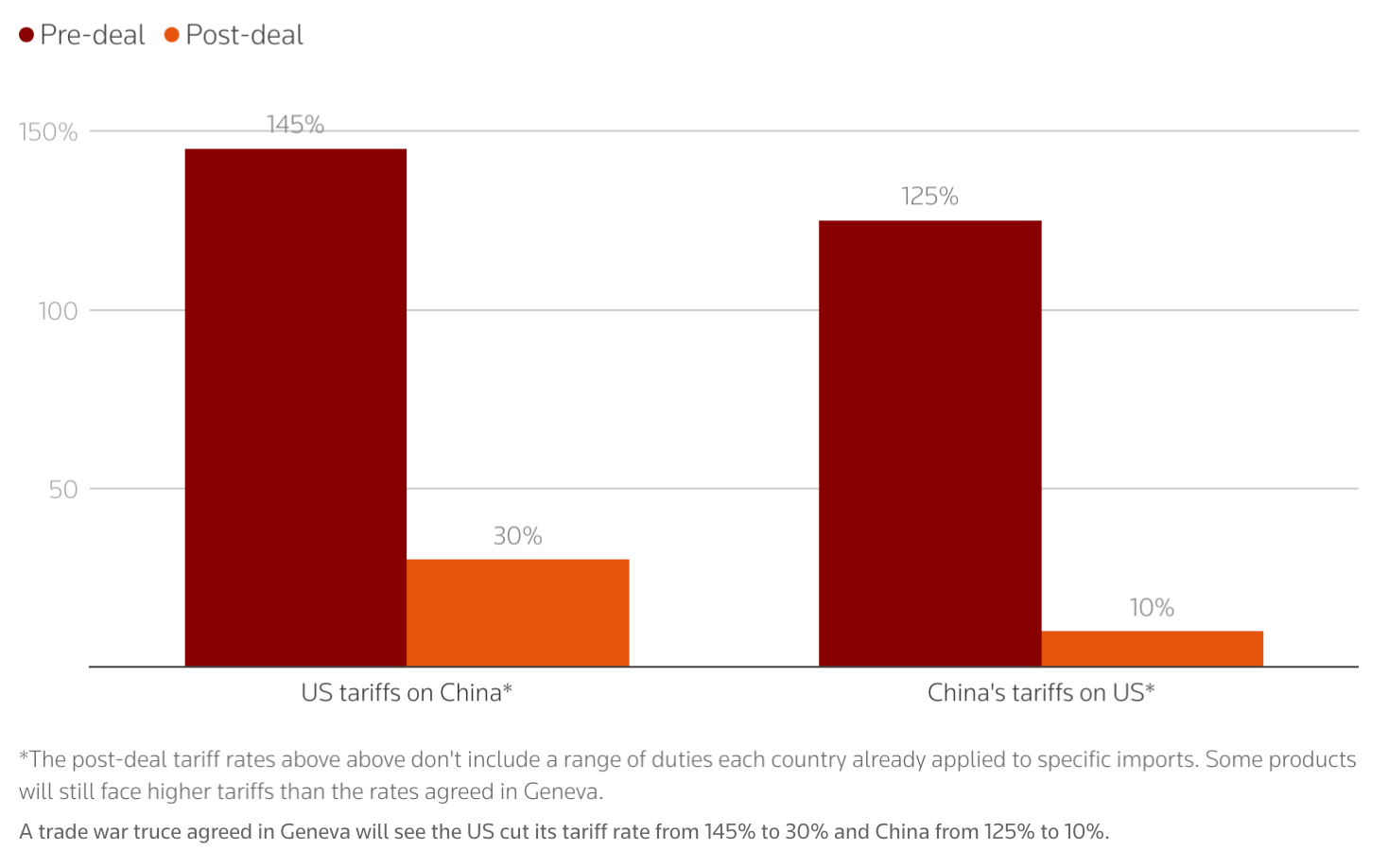

The U.S. and China have reached a temporary deal to ease tensions: a 90-day agreement that caps Chinese import tariffs at 30%—split between a 10% unified tariff and an additional 20% targeting fentanyl-linked goods. The move reflects pressure on Beijing to curb chemical exports fueling the U.S. opioid crisis. China also agreed to adopt non-tariff measures, though details remain undisclosed.

Markets soared on the news, with the S&P 500 jumping 3.3% and the Nasdaq surging 4.1% in a single day.

Is the U.S.-China trade war over? Certainly not. We expect high volatility to persist in the months ahead—defined as daily swings of ±3% in major stock indexes. That said, a quicker resolution remains possible, as the economic damage—especially to China—continues to mount.

As we've outlined in earlier publications, the market is already beginning to price in the endgame. And in our view, that endgame favors the U.S., with a resurgence in domestic manufacturing as the ultimate outcome.

The Q1 2025 GDP offers a glimpse of progress: U.S. gross domestic investment surged by 22% year-over-year. And this isn’t just a statistic—it’s playing out at the company level. According to FactSet, 78% of S&P 500 companies have reported positive EPS surprises. Even more telling, 45% of companies issuing Q2 EPS guidance have been positive—above the 5-year average (43%) and well above the 10-year average (38%)—despite the ongoing trade war.

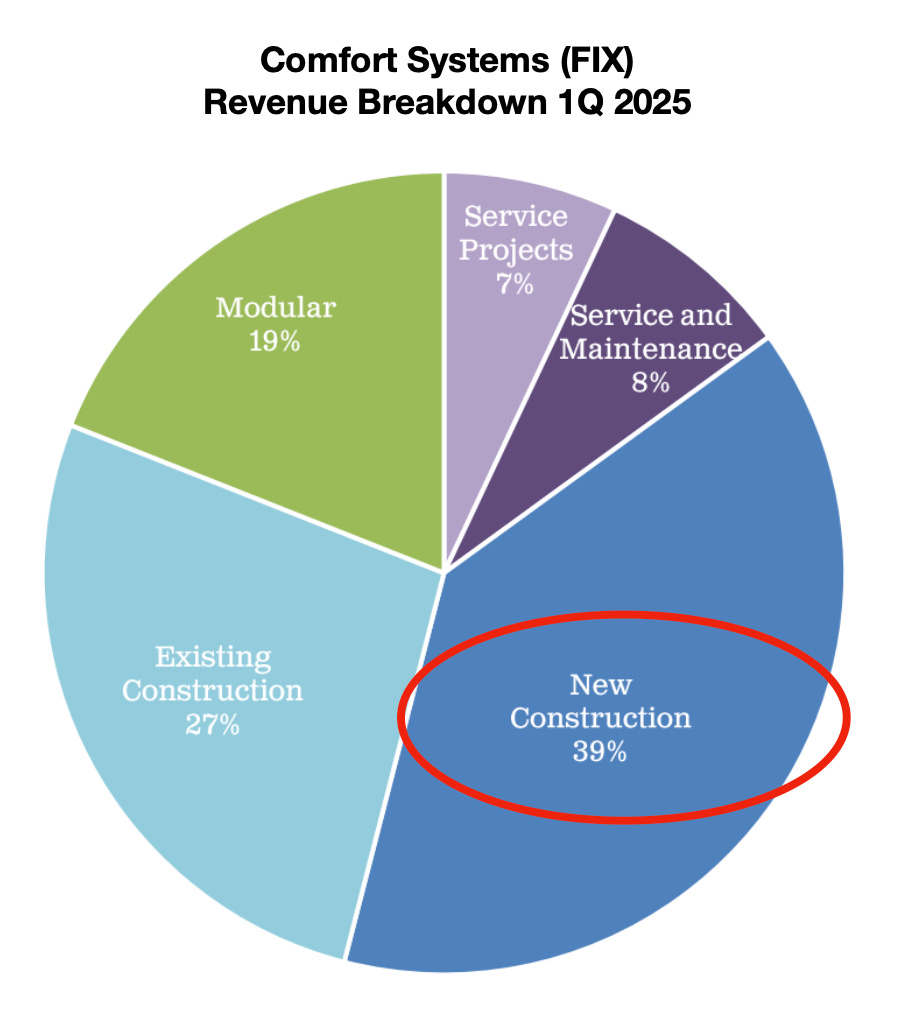

As we’ve noted, some companies are clear beneficiaries of rising domestic investment. Take Comfort Systems USA ( FIX 0.00%↑ ), for example. In Q1 2025, it reported 19% year-over-year revenue growth and a 15% increase in backlog. The company installs and maintains HVAC systems for both new and existing buildings—and 39% of its revenue comes from new construction. In other words, real investment is happening in the U.S.—despite the tariffs, or perhaps because of them.

So, what’s next?

Despite the volatility, several positive catalysts remain in play for the U.S. equity market.

First, trade negotiations are moving forward. The U.S. has reached temporary deals with both China and the UK, and smaller agreements are forming with other nations. Given that markets started from a place of deep pessimism on tariffs, any progress—even incremental—is likely to be viewed positively. Please also note, currently, President Trump is visiting the Gulf, and Qatar has just gifted the U.S. a $400 million jet.

Second, two of Trump’s major economic programs have yet to kick in: tax cuts and deregulation. As we've outlined, the next round of tax cuts is expected to focus on individuals—boosting consumer purchasing power and, over time, corporate earnings.

Deregulation may receive less media attention, but its impact is significant. Easing compliance burdens, accelerating project approvals, and increasing business flexibility will directly benefit companies in targeted sectors. These developments may come quietly, but they’ll matter.

Third, the long-anticipated Fed rate cut remains on the table. While the timing is uncertain, markets are watching closely.

Finally, corporate earnings momentum continues. As we saw in Q1 2025, most companies beat expectations. With strong investment trends and a 22% surge in gross domestic investment, there’s reason to expect more upside in Q2 results.

What are the risks?

The risks are exactly what you see in the headlines: a steady stream of macroeconomic data and analysis, and concerns over the U.S. debt level. These factors will continue to inject volatility into the market—mostly to the downside.

However, it’s worth noting that the greater risk may be on the upside. With multiple potential catalysts in play, the window to enter the U.S. stock market is narrowing as we move closer to year-end.

Our portfolio strategy

We see two major trends shaping the market: internal reform in the U.S.—including the revival of domestic manufacturing—and the rapid expansion of AI infrastructure. As a result, we favor companies with a strong U.S. focus, particularly those that sell or produce within the country. We want exposure to the U.S. because we believe it’s on track to emerge stronger than ever.

We also maintain a positive outlook on the utilities sector—one of the most underrated industries in the market. Utilities stand to benefit from both major trends: increased domestic manufacturing drives demand for energy and infrastructure, while AI-related data centers require massive, reliable power.

Happy investing.

Meme of the century

Investment talk aside, last week brought a surprising coincidence. Just six days after President Trump posted this meme, Cardinal Robert Prevost—a U.S. (and Peruvian) citizen—was elected Pope Leo XIV. Divine timing? Market signal? Mere coincidence? Either way, we may have just witnessed the meme of the century.