Chronicle of September 2024

All Eyes on China, We Look the Other Way

Luck, or shaman power?

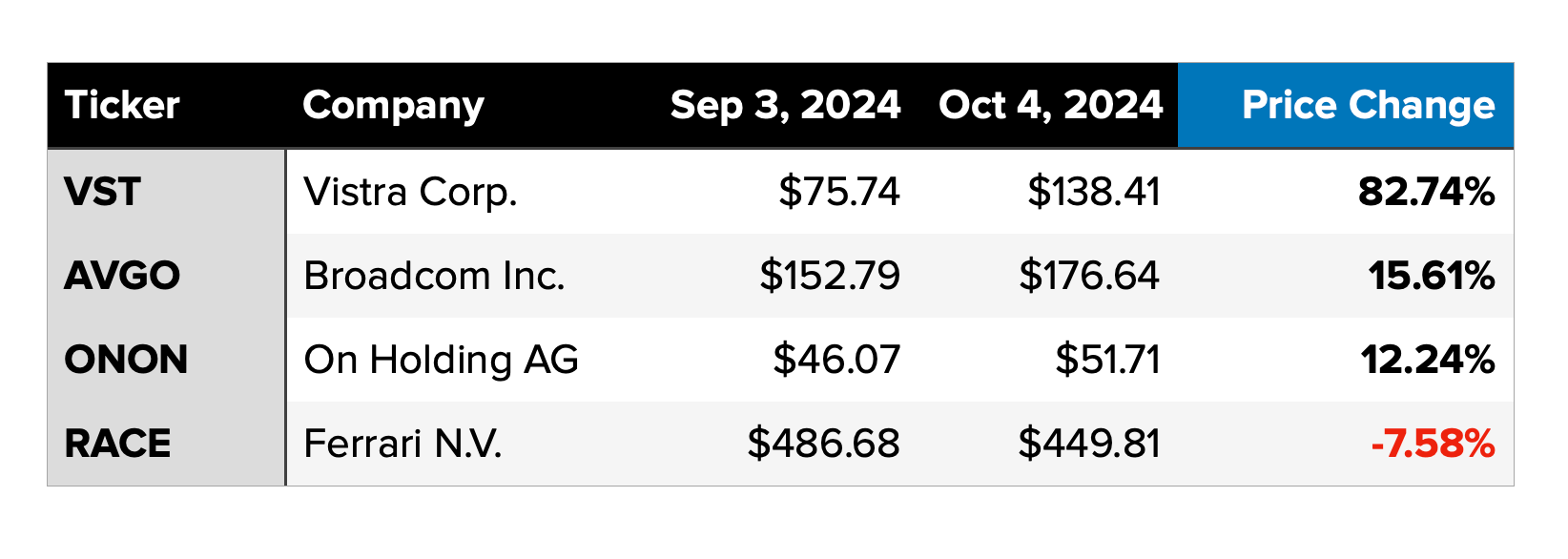

Before discussing about China market, we want to update our top stock holdings. Those companies were briefly outlined in our previous monthly chronicle (read here). Theses remain intact despite some of them have significantly gone up since our writing just a month ago.

Now, the serious part…

The Hang Seng Index (^HSI) has jumped 30% since China announced a series of stimulus measures to boost its weak economy in mid-September. Massive fund flows are pouring into China once again. However, we’re not following the herd, as we’re focused on assessing far more interesting sectors elsewhere.

According to Deutsche Bank, this time is different. The recent stimulus from China is more comprehensive and well-timed. Its size is substantial, potentially exceeding $700 billion, much larger than the stimulus package two years ago. It includes rate cuts, property credit easing, and policies to support the stock market. Furthermore, China experts believe Beijing will do whatever it takes to support the economy, including further stimulus in the hundreds of billions.

This is also considered good timing because the stimulus coincides with central banks around the world beginning to ease monetary policy. This favourable backdrop was absent during China’s previous stimulus two years ago.

With China’s stock market heavily shorted and fund flows shifting from Asia ex-China to China in anticipation of further stimulus, a short squeeze is forming, which is further boosting China’s stock market.

But is this stimulus enough to lift the struggling economy?

Although the current stimulus is the largest in nominal terms, it doesn’t seem substantial relative to GDP. The package could exceed $700 billion, making it the biggest ever and slightly larger than the Covid-19 stimulus in 2020. However, as a percentage of GDP, the current stimulus is relatively small—around 3.9% of GDP, compared to 4.5% during Covid-19 and significantly lower than the 12.5% during the 2008 Global Financial Crisis.

Whether this, or any additional stimulus, will be enough to boost the economy remains to be seen.

We’re looking the other way

Historically, China’s stock market has been appealing for traders due to its high volatility, but it’s not suited for long-term wealth building. The MSCI China Index, over the past 32 years since its inception, has delivered only a 1.27% annualized return—well below the broader MSCI Emerging Markets Index. China’s stock market also exhibits significant volatility, with a high standard deviation of 24.77%. Given these metrics, it's clear that China’s stock market may not be ideal for investors focused on long-term wealth growth.

There are many sectors and regions outside China offering better risk-reward opportunities. In the U.S. alone, sectors like utilities, materials, and consumer goods present significant potential. An impending electricity crisis is looming in the U.S., though many remain unaware. Utilities, the best-performing sector year-to-date, could see certain stocks continue their strong performance into next year.

Decades of green initiatives have pushed the materials supply chain to the brink, with nearshoring trends and rising geopolitical tensions only worsening the situation. This translates to more opportunities in the sector. The consumer sector also holds potential, especially from an M&A perspective, as building brands and securing distribution networks is costly, prompting larger players to favor acquisitions over in-house development.

Precious and industrial metals are also interesting. Despite the recent rise in gold prices, many gold producers are still undervalued. For the adventurous, there’s significant value to be found among Canadian and Australian miners, where untapped opportunities are plentiful.

The most rewarding paths are often the least traveled.