Chronicle of June 2024

The Consequences of Fake Inflation Data

Official inflation numbers are typically downplayed, leading people to make investment decisions based on inaccurate data. By the time they see the truth, it’s often too late; just look at the Argentinians, who’ve learned this the hard way over the past eighty years. Maybe it’s time to start diversifying your assets.

The Understated Inflation Data

As we discussed in the last Chronicle, official inflation data are often underestimated. By using the Big Mac Index as an imperfect proxy for inflation, it becomes evident that the actual inflation rates in most of the countries we track are significantly higher than the official figures suggest.

While Big Mac prices are certainly not an appropriate measure of a country’s overall inflation, as they represent a single product that most people don't consume daily, they do possess some favorable characteristics as an inflation measure.

First, the price of a Big Mac reflects the entire supply chain involved in its production: fuel prices, electricity, property rental costs, employee wages, flour, other food ingredients, and more. This comprehensive cost inclusion provides a broad economic snapshot.

Second, we can be confident that the price of a Big Mac is an efficient price, as it is determined by a well-established corporation with robust pricing mechanisms.

Lastly, Big Mac prices are comparable across countries, making them useful for cross-country inflation comparisons.

In contrast, official inflation numbers are often subject to statistical manipulation and selection bias, making them potentially less reliable than the more straightforward Big Mac Index.

The Bad Investment That Looks Good

Ironically, while people are usually aware that the prices of their daily necessities are rising faster than official inflation rates, many still base their investment decisions on these official numbers, directly or indirectly. This is particularly concerning in an era where governments frequently intervene in bond markets, distorting interest rates.

For example, those who primarily invest in government bonds may actually be eroding their own wealth. If you have a pension fund or are a member of a welfare program, be cautious. The distorted interest rates from these bonds mean your investments are not keeping pace with actual inflation. This leaves you vulnerable to losing purchasing power over time.

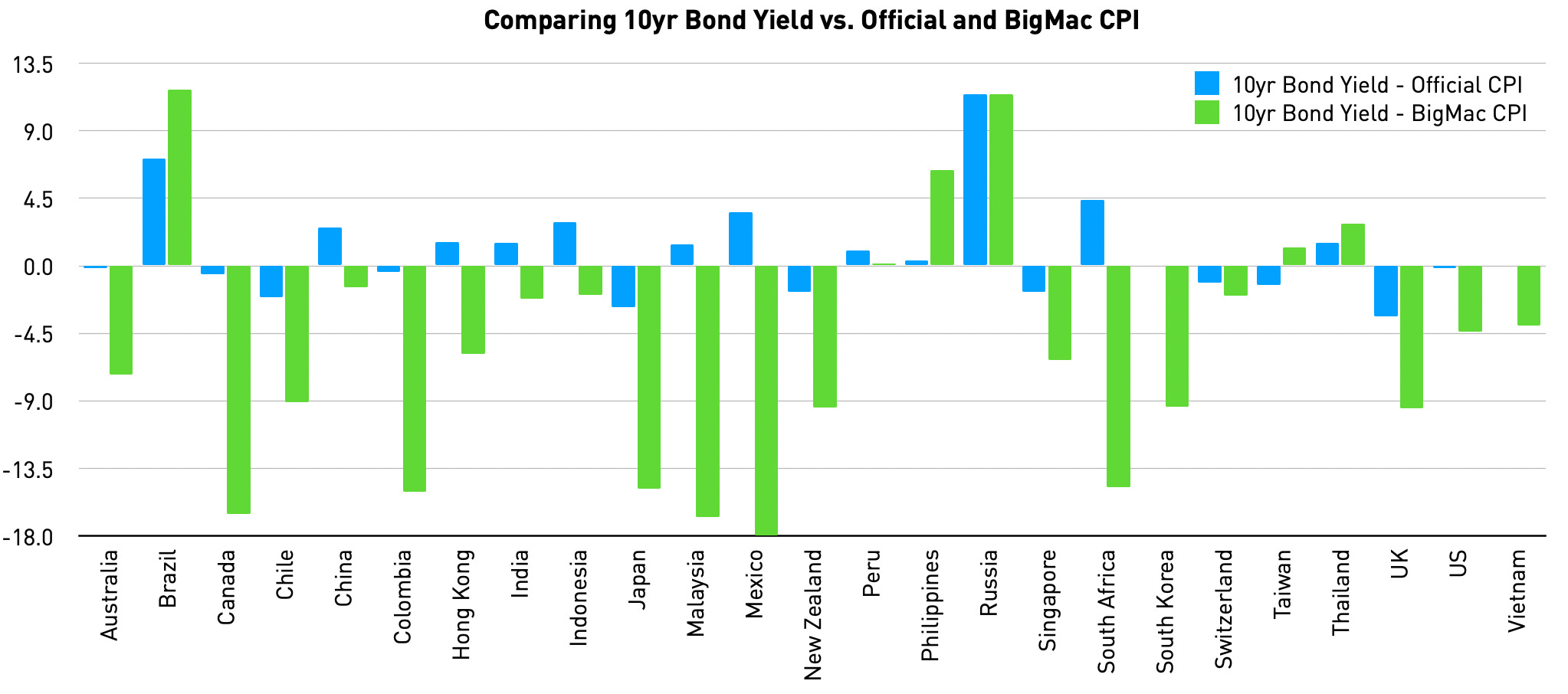

The following chart shows how the 10-year bond yields, a standard investment for pension funds and welfare funds in most countries, are actually far below the 'actual' inflation as represented by the Big Mac Index. In some countries, such as Mexico, the gap between the 10-year bond yield and actual inflation is alarming, reaching as much as 18%. This means that if a Mexican invests in Mexican bonds, they effectively lose 18% of their purchasing power per year. However, using the official inflation data, their investment would appear to generate a real return of 3.6% per year. Additionally, this return is further reduced because the interest income from government bonds is usually taxable.

Why is Inflation Data Understated?

There are several reasons. The technical reason is that inflation data is derived from too many items, which inherently lowers it. For example, in the U.S., inflation data is derived from over 80,000 items. Additionally, there are quality adjustments; if an item's price increases due to improved quality, this price increase doesn’t count as inflation.

But there are non-technical reasons as well. Since government spending is constantly increasing, governments need to keep borrowing (i.e., issuing bonds) or printing more money. Therefore, they have an incentive to keep inflation data low in order to maintain low interest rates and ease their debt burden.

Argentine War Against Inflation

No country has felt the harsh impact of inflation as profoundly as Argentina. Once a wealthy nation in the early 20th century, it has since descended into poverty. This decline was spurred by a succession of socialist leaders who implemented policies that began with rampant price controls and subsidies in the 1940s, followed by high-tax regimes and increased government spending on social programs. However, these measures proved unsustainable for Argentina. What ensued was decades of persistent high inflation that eroded the wealth of its populace.

Eight decades later, when the people had grown desperate with their country, they finally elected President Javier Milei, who dared to roll back decades-long populist policies. His actions ranged from cutting government expenditure, including popular social subsidies, to reducing trade tariffs. His austerity measures were undoubtedly painful medicine, but they eventually saw a week without inflation for the first time in 30 years.

Diversify Away

Argentina is just one example. High inflation and increasing taxes—whether explicit or implicit—are prevalent in many other countries, from Kenya to Indonesia, and beyond.

Government policies and regulations are beyond our control, and figures like Milei are rare. Therefore, it's crucial to take charge of our personal wealth ourselves. One of the first steps we can take is to diversify our assets across different locations.

Gone are the days when it was common to concentrate all assets within a single country. Now, it's essential to be vigilant about real inflation, taxation, and the privacy of our assets.