Chronicle - Jan 7, 2024

What’s in Store for 2024

Events in the first week of 2024 provide a sneak peek into the year ahead.

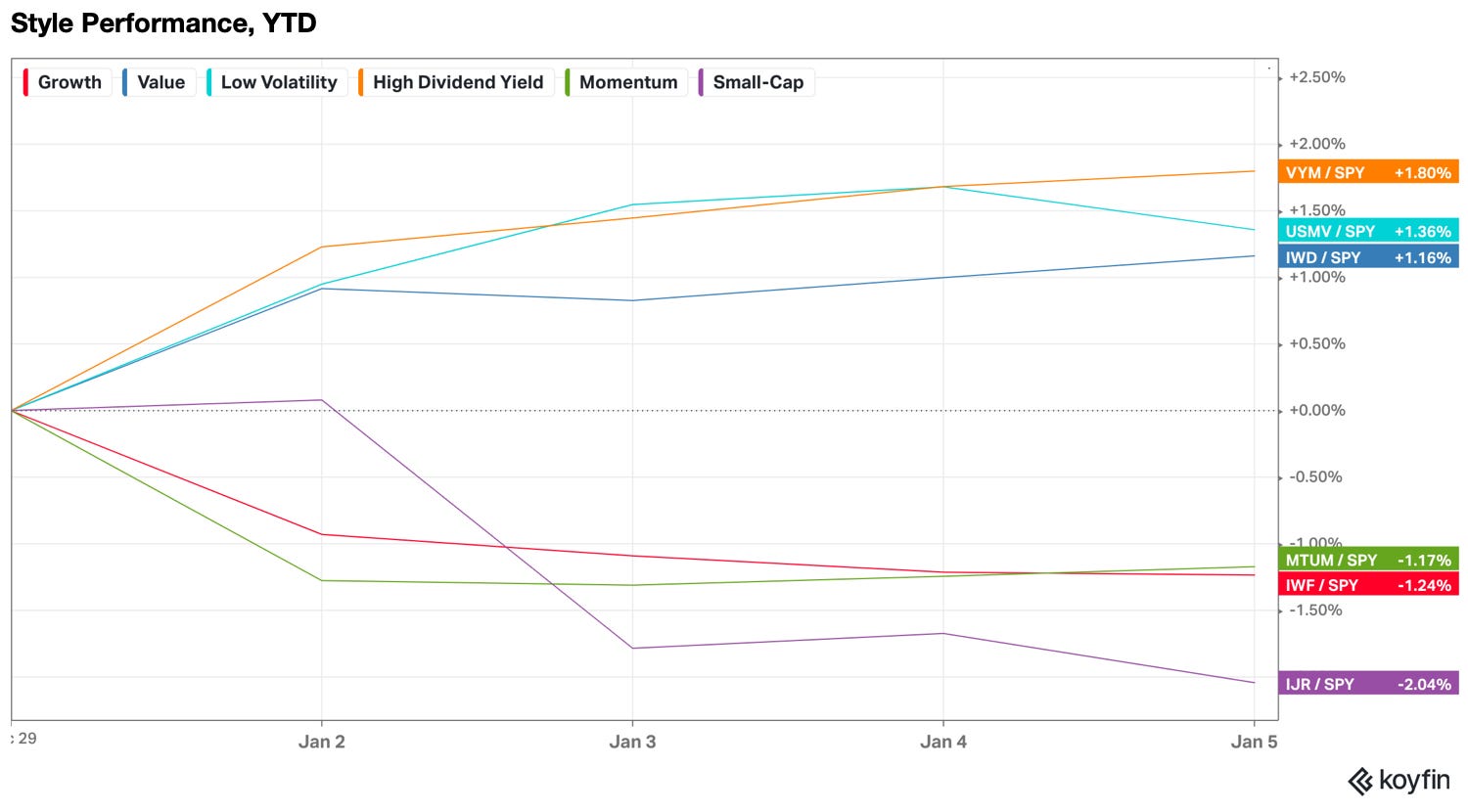

The Fed’s (Delayed) Pivot

The Bureau of Labor Statistics stated on Friday that the U.S. added 216,000 jobs in December, while the unemployment rate remained at 3.7%. This was more than the market's expectation of 175,000 jobs. These figures indicate that there is no immediate need to lower interest rates; in other words, “higher rates for longer”.

The market's reaction is obvious. Some participants correctly predicted that the results would be more robust. Since the beginning of the year, the 2-year yield has climbed by +14 bp, as have other longer time frames.

The stock market reacted similarly. Investors' risk appetite has waned as they seek safe companies and avoid riskier growth stocks.

This is in stark contrast to the market's expectation of six rate cuts in 2024 last month. Based on last week's data, that anticipation may not hold. Instead, the Fed's own prediction of three rate cuts may be more accurate.

Volatility will result from the expected mismatch between the market (6 rate cuts) and the Fed (3 rate cuts). Furthermore, the Fed estimate was calculated using the median of individual Fed official expectations (called the dot-plot). As every Fed official claims to be data-driven, the dot-plot number is only a rough guideline.

So, expect multiple swing moves between risk-off and risk-on. Whatever the Fed does, there are always reasons to sell or to buy. Imagine this: if the Fed cuts three times as the dot-plot suggests, the market might be disappointed because the Fed may not finish the job—to kill inflation. But if the Fed cuts six times as much as the market expects, they might be disappointed too, because it means the Fed sees the economy as worse than what the market expected.

If you are confused, that’s natural. Rest assured, the U.S. (and world) economy is in the hands of 400 Ph.D.s working diligently at the Fed.

Escalating Geopolitical Tensions

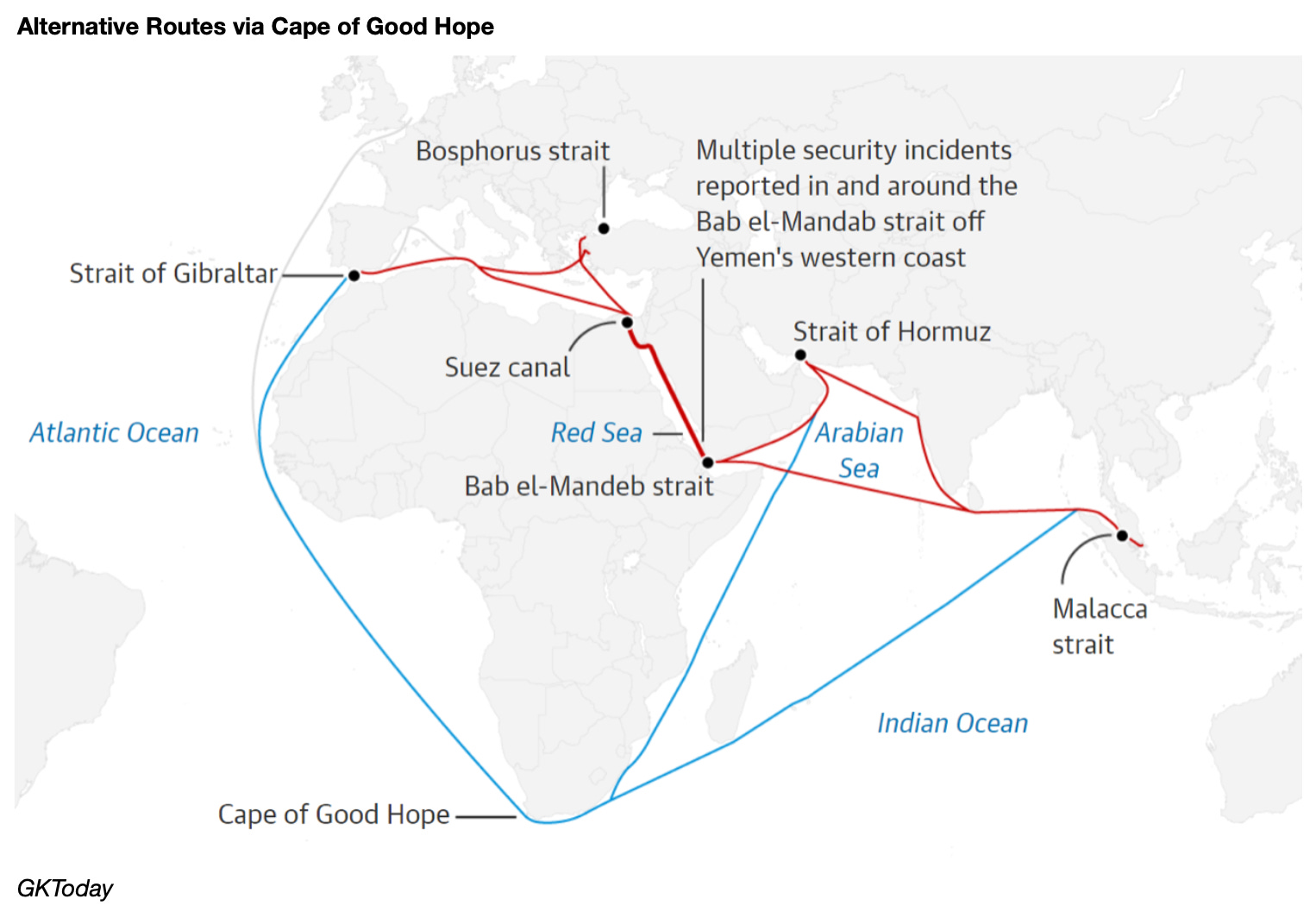

The Fed is not the only source of volatility. Last week, shipping giant Maersk extended its diversion of vessels from the Red Sea for the foreseeable future due to the attacks by Houthi militants. Previously, other shipping companies had done the same.

Diverting vessels from the Red Sea means a longer route via the Cape of Good Hope in southern Africa. This adds 10 days of sailing time and 5000 kilometers (+30%) to the route from Asia to Europe. It represents a huge cost rise.

To make matters worse, the detour does not imply a safer route. Last week, Somali pirates captured a ship, and Indian naval commandos saved the sailors on board. It turns out that navy ships from several countries have been shifted from the Somali coast to the Red Sea.

If the Red Sea is not enough, there are several other hot spots around the world that could potentially disrupt international trade and prices, from Guyana to China to Ukraine.

But rest assured, President Biden conveniently suggests that the U.S. can afford two wars (in Ukraine and the Middle East). Janet Yellen, the Treasury Secretary and former Fed chair, fully supports this stance.

Anticipating the Most Important Election Ever

Maybe what we need is a U.S. election that hopefully brings peace and prosperity, not chaos. That most-awaited election will be held in November. However, at this early stage, predicting the election results remains uncertain.

What is certain is that there will be a lot of noise and anger. Every scenario is possible, including the rematch between Biden and Trump or the introduction of a third-party candidate.

It will be a fun year.

IPO — Performance