Chronicle - Feb 21, 2025

Should You Wait to Buy USD?

Many investors looking to allocate capital into U.S. assets often wait too long for USD weakness before making their move. But is this the right approach? Should investors take a different strategy?

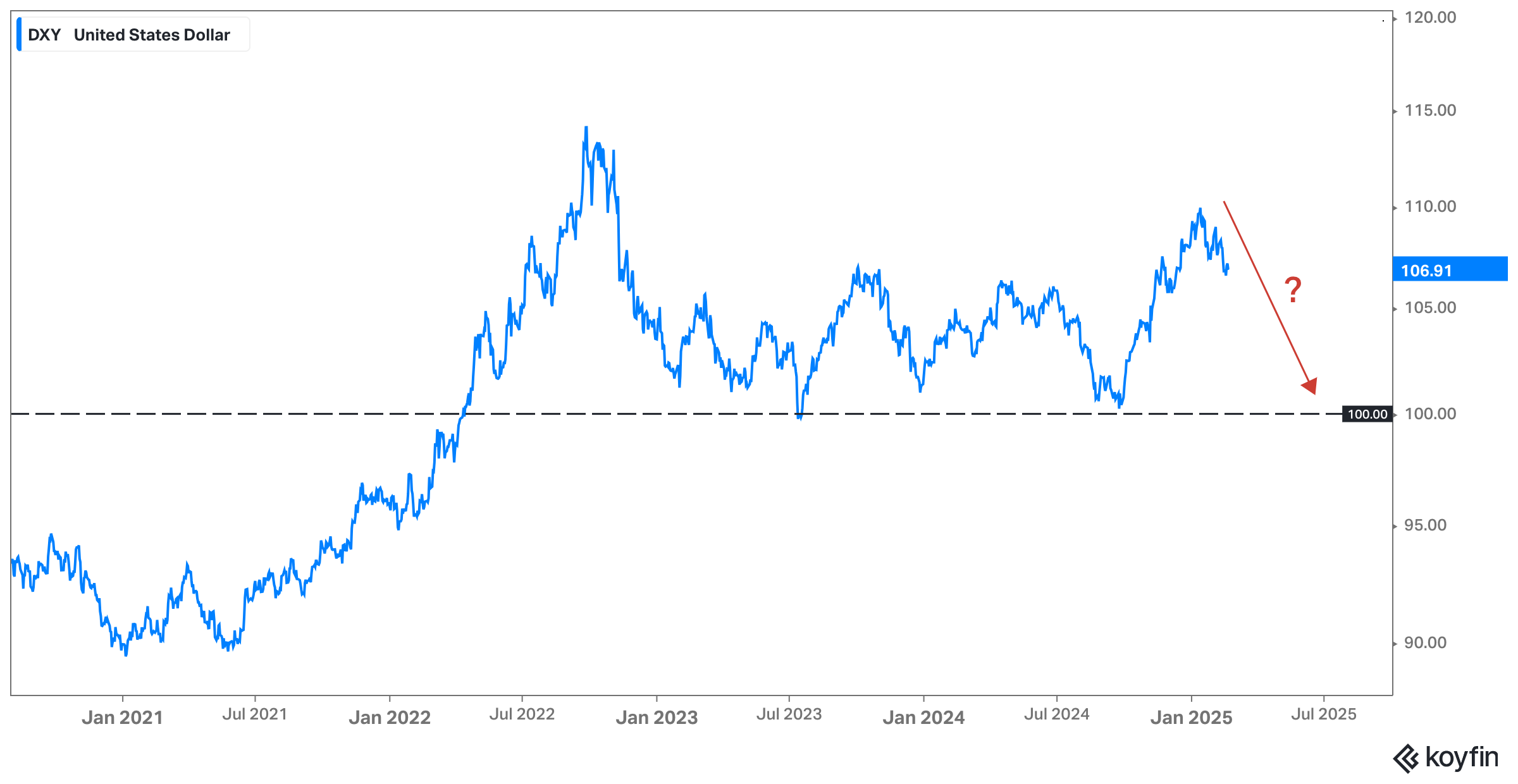

The USD index (DXY) is currently showing a downward trend. Many believe a weaker USD is necessary for the U.S. to regain manufacturing competitiveness. But does this mean the dollar will continue to weaken?

Understanding the USD Index (DXY)

The DXY measures the value of the U.S. dollar relative to a basket of six major currencies, with the euro carrying the most weight at 57.6%, followed by the Japanese yen (13.6%), British pound (11.9%), Canadian dollar (9.1%), Swedish krona (4.2%), and Swiss franc (3.6%). Created in 1973 with a base level of 100, a reading above 100 indicates the dollar has strengthened compared to that year, while a value below 100 signals depreciation.

Since the index is largely influenced by the euro, its fluctuations primarily reflect the strength or weakness of the Eurozone relative to the U.S.

Implied Interest Rates and the Dollar

According to MacroMicro, an economic research platform, implied interest rates are a way to estimate where future interest rates might be based on market expectations. These rates are calculated from short-term interest rate futures. For example, if a Fed funds futures contract is priced at $96, the expected interest rate is 4% (100 - 96).

When the difference between U.S. and Eurozone implied interest rates grows, U.S. assets become more attractive to investors, leading to more capital flowing into the U.S. and increasing demand for dollars, which strengthens the DXY index. On the other hand, if the rate gap narrows, investment may shift toward the Eurozone, lowering demand for dollars and weakening the index.

We are now seeing the rate gap widens, meaning DXY trajectory is to strengthen, until mid-year.

The Known Unknowns

Beyond implied interest rates, other factors make a stronger USD more likely:

Foreign Direct Investment (FDI)—the capital foreign companies spend in the U.S.—has remained strong since 2021, likely driven by bipartisan onshoring policies that incentivize foreign investment. Higher FDI increases demand for USD, as foreign companies need to convert their currencies to fund operations on U.S. soil.

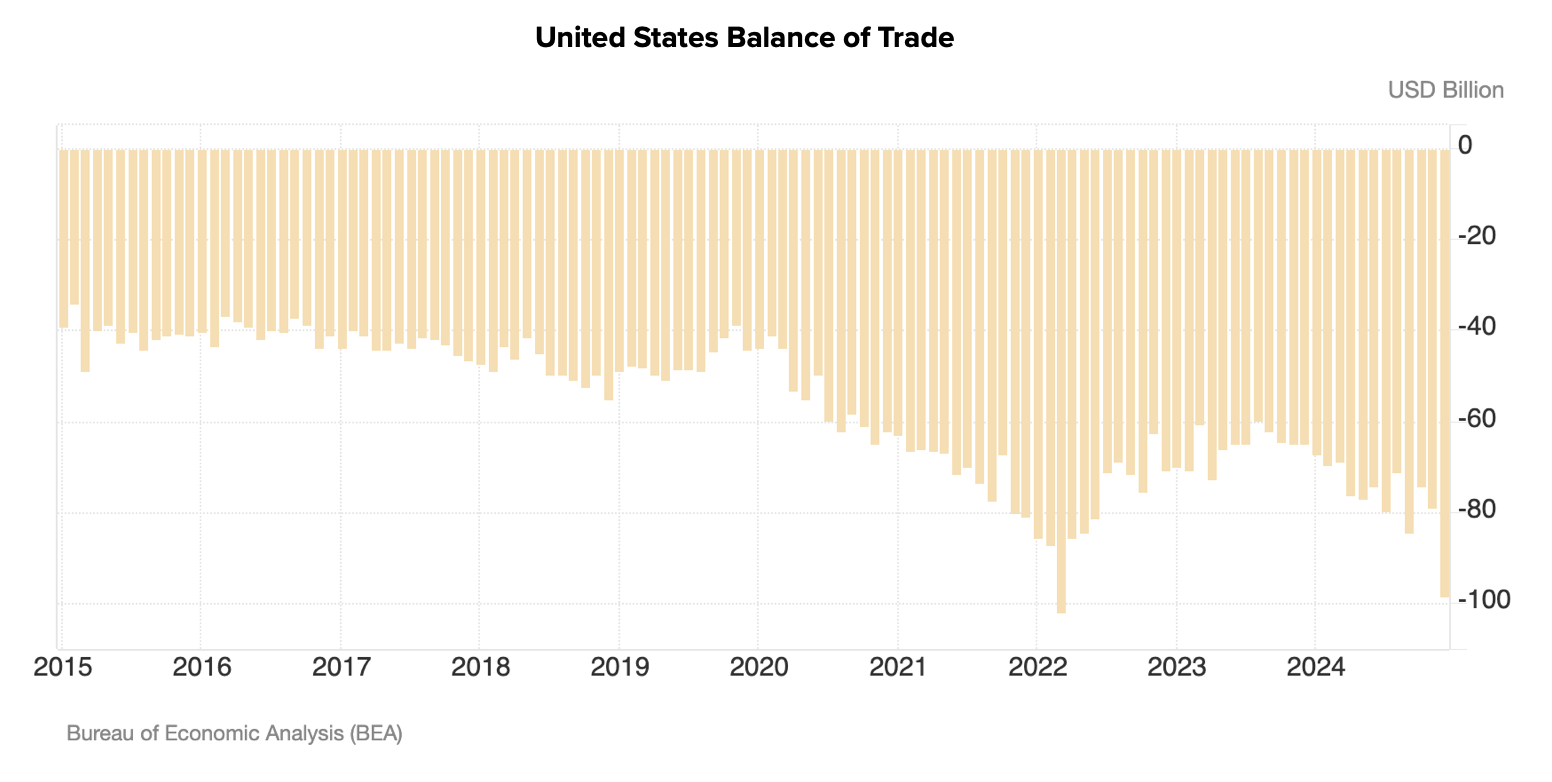

For decades, the U.S. has been known for its large trade deficit. Since it imports more than it exports, it sends more USD abroad. However, Trump's reciprocal tariff policy could reduce imports by imposing higher tariffs, ultimately shrinking the trade deficit. A lower trade deficit means less USD circulating globally, which, in turn, could drive up the dollar’s value due to reduced supply.

Lastly, and this is a big IF, if the Trump administration successfully reduces government debt, the Fed would no longer need to buy Treasuries or create more USD. This would halt the supply of new dollars, driving up the value of the USD.

Over the past 15 years, the DXY has risen despite the increasing supply of USD. What would happen if the supply of USD stopped increasing?

The Key Misconception: DXY vs. Your Local Currency

Many investors focus too much on the DXY, assuming its movements directly correlate with their local currency. However, DXY measures USD against a specific basket of currencies, not all global currencies. A decline in DXY does not necessarily mean your local currency strengthens against USD, or vice versa. It is crucial to analyze how USD performs against your specific currency instead of relying solely on the DXY.

So When to Buy USD?

Timing the market is difficult, and waiting indefinitely for USD weakness may not be the best approach. Instead of relying on macroeconomic forecasts or the DXY, a disciplined Dollar Cost Averaging (DCA) strategy ensures consistent USD accumulation. This approach helps mitigate market volatility and reduces the risks of mistiming your investment decisions.